New Zealand is moving to a single AML/CFT Supervisor: Here’s what it means for you.

Where things stand today

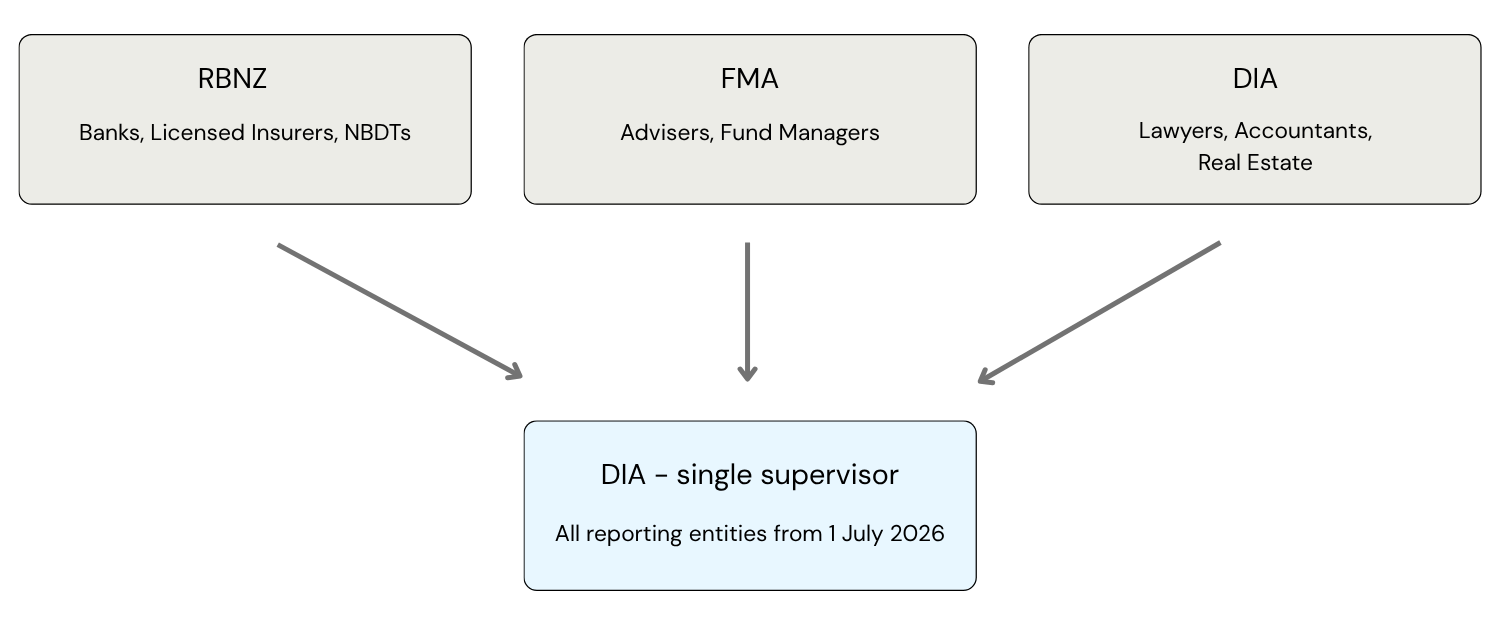

Right now, Anti-Money Laundering & Countering Financing of Terrorism (AML/CFT) supervision in New Zealand is split across three regulators depending on your industry:

• The Reserve Bank of New Zealand (RBNZ) looks after banks, life insurers and non-bank deposit takers.

• The Financial Markets Authority (FMA) covers financial advisers, fund managers, brokers and other financial markets participants.

• The Department of Internal Affairs (DIA) supervises everyone else: lawyers, conveyancers, accountants, real estate agents, casinos, trust and company service providers, high-value dealers, and financial service providers that don’t fall under the other two.

Each supervisor publishes its own guidance and knows its sectors well. The model has been in place since the AML/CFT Act came into force in 2013.

One supervisor from 1 July 2026

From 1 July 2026, the DIA becomes the single AML supervisor for every reporting entity in New Zealand.

This is now law. The AML/CFT (Supervisor, Levy, and Other Matters) Amendment Bill passed in May 2026, and the change kicks in within a matter of weeks. The DIA, FMA and RBNZ have been planning the handover together, with the aim of keeping disruption to a minimum.

It’s the biggest structural change to the regime since it began.

Why one supervisor?

The move is part of a wider reform designed to make AML/CFT simpler for businesses to work with. Having one supervisor means one set of guidance and a single point of contact, whatever industry you’re in. It also gives the DIA visibility across the whole regime, which makes it easier to spot patterns and respond as risks shift between sectors.

It depends who supervises you now

If you’re already with the DIA (lawyers, accountants, real estate agents and most other reporting entities), not much changes on 1 July. Same supervisor, same relationship. Over time you should see the benefits of a regulator with a wider view of the sector.

If you’re currently with the FMA or RBNZ, your supervisor moves to the DIA, and your obligations under the Act stay exactly the same. You will see new points of contact, new reporting channels and updated guidance as everything comes under one roof.

What’s not changing

Quite a lot, actually:

• Your obligations under the AML/CFT Act

• The need for a current risk assessment and compliance programme

• Customer due diligence, ongoing monitoring, suspicious activity reporting, annual reports and independent audits

This is a change to who supervises you, not what’s expected of you.

Worth doing before 1 July

There’s no need to overhaul anything, but a few things are worth doing before 1 July.

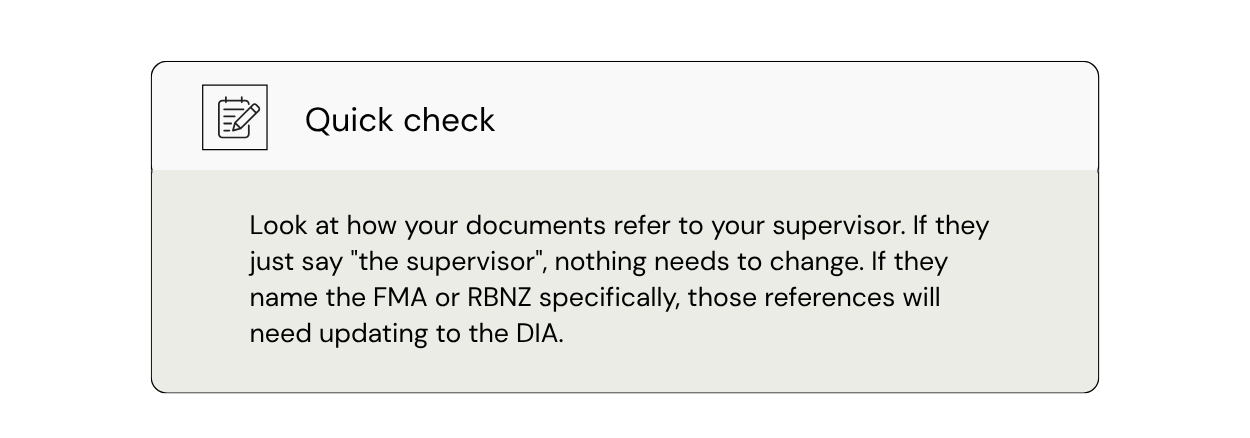

Check your documentation is up to date. If your risk assessment or compliance programme is due for a review, get it done sooner rather than later.

Keep an eye out for DIA communications about the transition, and make sure the right person in your business is receiving them. That’s not just your compliance officer – senior managers and board members should be across the change too, given their oversight responsibilities under the Act.

And remember this is just one part of a bigger reform programme. More changes are on the way, including an industry levy and a final omnibus bill.

Our take

For most reporting entities this is a good change. One supervisor, one set of guidance, and a more consistent experience across the board. There’ll be an adjustment period while the DIA takes on its new responsibilities, but it’s a step in the right direction.

If you’re not sure how the transition affects your business, or your risk assessment and compliance programme is due for a review before 1 July, the team at AML Solutions can help.

—————-

Head of Consulting, BCOM, CAMS

Brandon is an experienced AML/CFT professional with a strong background in accounting, risk and compliance. He brings over a decade of AML/CFT experience in New Zealand, dating back to before the establishment of the AML/CFT regime.

Throughout his career, Brandon has worked across multiple sectors, including banking, payments and managed investment schemes. Prior to joining AML Solutions, he served as the AML/CFT Compliance Officer for several large and mid-sized reporting entities. Brandon has led numerous AML/CFT remediation projects and has extensive experience coaching businesses through the practical challenges of complying with the AML/CFT Act.